- Category

- War in Ukraine

The War That Broke Russia’s “Fortress Economy”

For years, analysts spoke of “Fortress Russia”—an economy insulated by vast reserves and conservative fiscal policy. Then, what began as a full-scale military invasion of Ukraine has evolved into a full-scale degradation of Russia’s economic system.

- Authors

-206008aed5f329e86c52788e3e423f23.jpg "Photo of Oleksandr Moiseienko")

Before February 24, 2022, Russia’s economy was heavily oriented toward commodity exports but maintained some of the most stable macroeconomic indicators among G20 countries—one of the lowest levels of public debt, relatively low inflation, a consistent budget surplus, and steadily growing reserves.

Moscow’s full-scale war against Ukraine, now entering its fifth year, has reshaped Russia’s economic trajectory, exposing structural vulnerabilities that can no longer be offset by accumulated reserves, hydrocarbon export revenues, or conservative fiscal policy.

How Russia built its “fortress economy”

In analytical circles prior to the events of four years ago, Russia’s economy was often informally described as “Fortress Russia.” Although Russia’s 2014 invasion of Ukraine was condemned by the international community, it did not place Russia—or its economy—in the same category as countries such as Iran or Venezuela.

Sanctions were formally imposed to limit Russia’s technological capacity and access to global financial markets. For many G20 countries, losing such access would have been a painful shock. However, Russia—benefiting from a continuous and substantial inflow of foreign currency from hydrocarbon exports and facing no meaningful electoral accountability—methodically reduced its public debt and eliminated its reliance on external capital markets.

Other defining features of Russia’s economic model included tight fiscal policy, de-dollarization of international reserves, and the accumulation of funds in the National Wealth Fund, where excess oil revenues were set aside for a “rainy day.”

That day effectively arrived on February 24, 2022. After failing to achieve its initial objective of capturing Ukraine within weeks, Russia shifted its economy onto a wartime footing and began spending its reserves to sustain a prolonged and exhausting war.

How Russia spent in 4 years what it had accumulated over 15

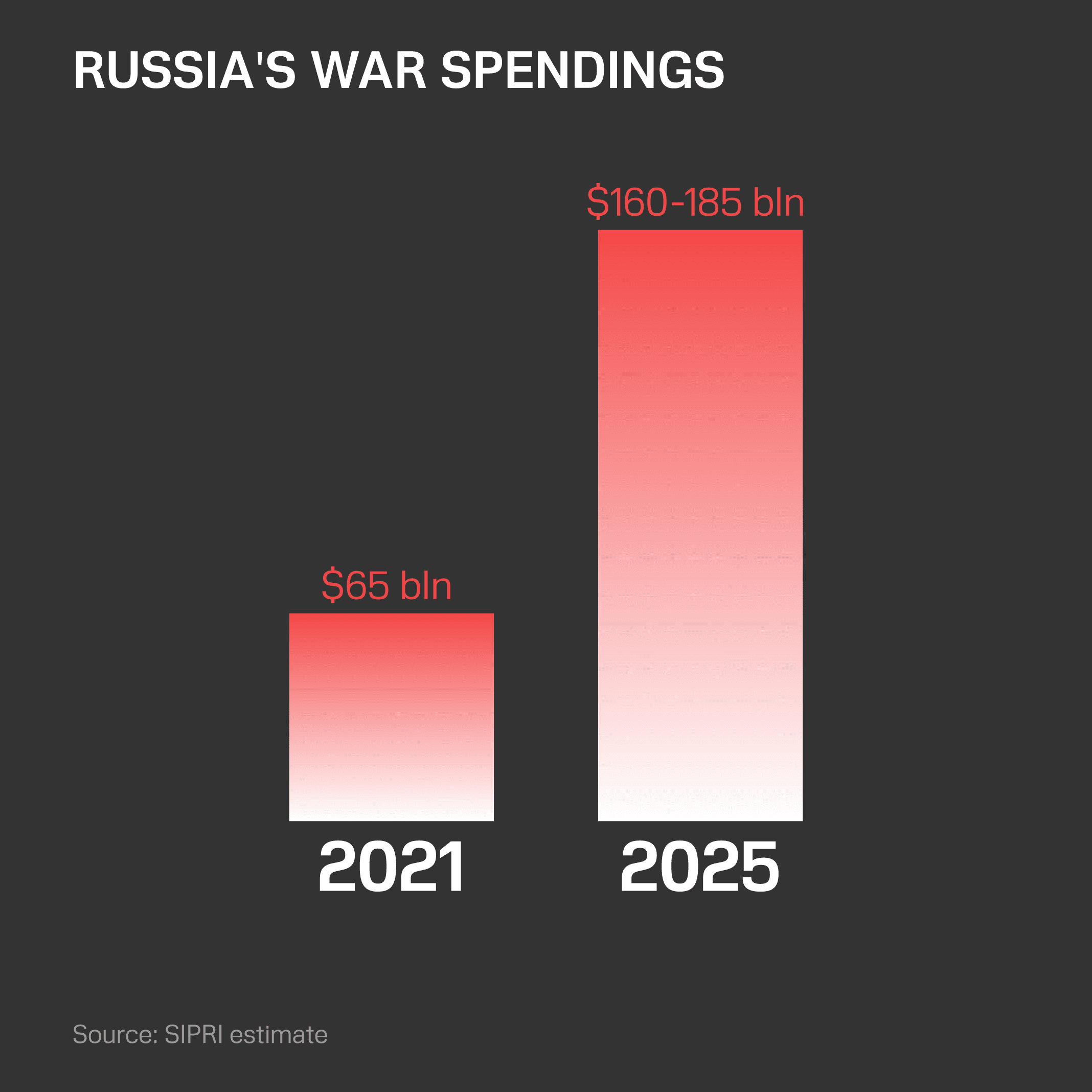

In 2021, Russia’s military budget amounted to approximately $65 billion. By 2025, it planned to spend $160 billion. The traditional budget surplus turned sharply into a deficit in 2022, and the fiscal gap has widened year after year despite government efforts to extract maximum tax revenues from Russian businesses. In 2025, the consolidated deficit of all levels of government reached roughly $100 billion—one of the highest figures in the post-Soviet period.

Two-thirds of the gap was generated by the federal budget, which exceeded its planned deficit fivefold. Regional budgets also posted a 20-year record deficit of approximately $20 billion.

The sharp increase in spending on defense, security, and support for the arms industry has been financed through domestic borrowing, tax hikes, and accumulated reserves. However, by the end of 2025, the National Wealth Fund's liquid assets had declined to around $50 billion—roughly the level it stood at in 2008.

Why GDP growth does not always reflect economic success

In 2024, Russia’s economy grew by more than 4%. At the same time, entire sectors—such as coal—were going bankrupt, while major light-industry manufacturers that had operated in Russia for decades failed to withstand competition and exited the market. The pattern of GDP growth began to resemble that of the Soviet era.

Those who lived through its final years remember the shortage of essential consumer goods, despite the USSR's formal ranking among the world’s leading economies.

Amid tightening sanctions and the gradual loss of key export markets, statistical economic growth was largely driven by a sharp increase in government spending, primarily in defense and related industries.

Fiscal and quasi-fiscal expansion—including loans issued by state banks—supported the arms industry, whose products are consumed daily on the Ukrainian front. This stimulated short-term economic activity in sectors such as machinery manufacturing, metallurgy, and chemicals, which are directly integrated into military production chains.

However, such growth had limited multiplier effects for the civilian economy and was not accompanied by improvements in labor productivity, investment in high-tech sectors, or expansion of export potential.

Thus, current GDP dynamics reflected a redistribution of resources toward wartime needs rather than sustainable economic development. By 2025, growth had stalled, and the Russian economy effectively entered a period of stagnation.

International reserves are growing—on paper

By the end of 2025, Russia’s international reserves had reached the equivalent of $800 billion—$170 billion more than at the beginning of 2022.

However, the devil is in the details. The increase was driven primarily by the revaluation of gold holdings within the reserve structure.

The actual capacity of these reserves to serve as a stabilization buffer is significantly limited. A substantial portion of the Central Bank’s assets—estimated at $300–400 billion—remains immobilized in Western jurisdictions, making them unavailable to cover budget deficits or conduct currency interventions.

Against this backdrop, the National Wealth Fund has become a key domestic source of financing for fiscal shortfalls. Since 2022, its liquid portion has steadily declined, accompanied by record gold sales.

While the nominal volume of international reserves remains relatively stable, the financial buffers available for operational use are gradually being depleted. Resources accumulated under the banner of macro-financial stability have effectively been converted into instruments for sustaining ongoing budget needs during a protracted military conflict.

Rising tax burdens and forced capital repatriation

When faced with a budget deficit and closed access to external borrowing, governments have limited options beyond expenditure cuts. In addition to inflationary tools, this means increasing fiscal pressure — raising taxes, forcing capital repatriation, or nationalizing assets. Since early 2022, Russia has actively used all of these instruments.

From 2023 onward, the country has seen a steady increase in the tax burden on large enterprises, including one-time “voluntary contributions” from major businesses, higher profit taxes for certain sectors, and an expanded tax base. In 2025, Russia raised VAT to 22%, placing it among countries with the highest rates of this tax. At the same time, simplified tax regimes have been significantly reformed, affecting small and medium-sized enterprises.

Business uncertainty is compounded by the need to continually adapt to sanctions, including the risk of secondary sanctions, restrictions on imports of critical technologies, and disrupted logistics chains. Together, these trends create an environment of rising operating costs, diminished investment attractiveness, and limited access to external financing.

Meanwhile, Russia’s Prosecutor General’s Office has actively reclaimed assets privatized in the 1990s. The list of seized assets—from the largest canned food producer to one of Moscow’s major airports—continues to grow. In many cases, these assets do not remain in state hands for long but are transferred to businessmen close to Putin. Despite these measures, the budget deficit continues to expand year after year.

Energy: from global expansion to forced discounting

Before the full-scale invasion, the energy sector played a key role in ensuring Russia’s macro-financial stability. Major state energy companies were viewed as instruments of geoeconomic influence, with strategic plans to expand capitalization and strengthen global market positions. Oil and natural gas exports generated more than half of the country’s foreign currency earnings and a significant share of federal budget revenues.

In 2008, Alexey Miller, head of the Russian state-owned energy corporation Gazprom, predicted the company’s capitalization would reach $1 trillion within seven to eight years. By 2025, its market value did not exceed $40 billion — largely due to the Russian invasion of Ukraine.

Following the loss of traditional markets, particularly in the European Union, Russia was forced to redirect exports toward Asia, often by offering significant price discounts. The company has posted persistent losses, reduced staff, and cut production.

A similar fate may await Russia’s oil giants, which are now compelled to sell crude at substantial discounts and rely on a shadow fleet of aging tankers.

Energy exports are increasingly used not as a tool for building reserves but as a means of financing ongoing budgetary needs in a wartime economy. Rising logistics, insurance, and fleet maintenance costs—combined with discounted sales relative to global benchmarks—significantly reduce the effectiveness of energy exports as a pillar of macroeconomic stability.

Banking: high rates and mounting credit risks

Amid rising inflationary pressures and depreciation risks triggered by wartime fiscal expansion, the Russian Central Bank has been forced to maintain a tight monetary policy. Between 2023 and 2025, the key interest rate averaged around 17%—unusually high for a country with a current account surplus.

The rising cost of money has affected both corporations and households. Russians are increasingly turning to microfinance institutions and accumulating debt. Average credit card interest rates can exceed 50%, while mortgage rates have reached 20%, effectively freezing the mortgage market.

Many Russian companies were unprepared for such elevated rates, leading to declining profitability and losses. Even oligarchs traditionally loyal to the Kremlin have publicly criticized the Central Bank’s tight monetary policy.

Meanwhile, banks are increasingly required to finance government debt, crowding out private lending. Put simply, banks are compelled to purchase federal government bonds (OFZs) rather than channel available liquidity into loans. With external borrowing effectively closed off, OFZs have become the last remaining instrument for covering fiscal shortfalls—a temporary patch that does not resolve the problem in the long term.

There is also growing concern over the accumulation of non-performing loans within the banking system. Banks have been compelled to subsidize defense enterprises that are not always profitable, and in the future, state banks themselves may require support from the federal budget—the same budget they are currently propping up.

Arms industry: Showcase growth with systemic risks

Between 2022 and 2025, Russia’s arms industry became the main beneficiary of budget expansion and one of the few sectors to demonstrate significant production growth.

Despite this surge, systemic issues—including modernization and profitability—remain unresolved. Russian defense plants have continued importing foreign equipment and components to expand output.

Previously undisclosed record export contracts for helicopters and aircraft have recently been published. However, the actual capacity of Russia’s arms industry to fulfill these contracts—and whether they can sustain the sector’s financial stability—remains questionable.

Despite heavy financial injections, key enterprises operate on the brink of bankruptcy, and some export contracts are unprofitable due to rising production costs. Delays in budget financing, restricted access to credit, and disrupted supply chains have led to mounting inter-enterprise debt, increasing the risk of payment crises and supplier bankruptcies.

Moreover, growing dependence on imported components and technologies from third countries, particularly China, creates new external vulnerabilities under the sanctions regime.

Most critically, the majority of defense output is consumed in ongoing combat operations, generating no long-term added value for the economy and failing to produce sustainable macroeconomic benefits or improve overall living standards.

Social dimension: Inflation, debt, and wartime mobilization of households

Despite official rhetoric about macroeconomic stability and adaptation to sanctions, the socio-economic consequences of the prolonged war are increasingly felt at the household level.

When Putin speaks of Russia’s “sovereignty gains,” another reality unfolds: supermarkets attach anti-theft devices to butter, and a trending topic on Russian social media is the rising price of cucumbers—once a staple, now increasingly unaffordable for many.

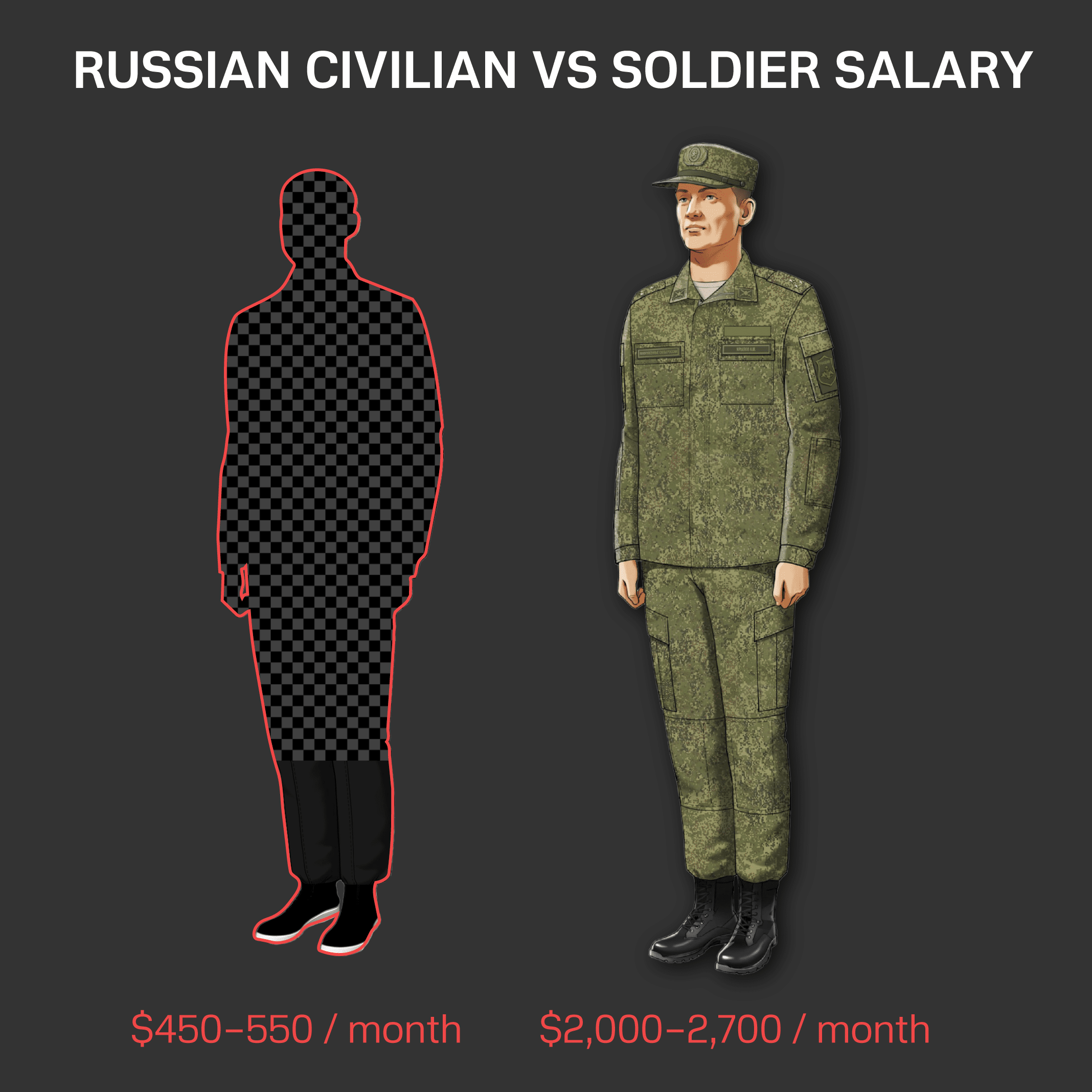

In these conditions, rising living costs are not matched by real income growth. Mounting financial strain and a deeply rooted sense of nihilism push many Russians toward quick earnings on the Ukrainian front. As a result, Russia remains able to deploy around 30,000 soldiers per month to Ukraine.

A significant segment of Russia’s economy now revolves around these 30,000 contract soldiers. They receive monthly pay and a $20,000–30,000 signing bonus. They spend their earnings; if they die, their families receive compensation payments. All of this remains possible—albeit with growing strain—because Russia continues to earn hundreds of billions of dollars from hydrocarbon and other resource exports.

At the same time, the leadership’s ambitions to prolong the war are not aligned with the economy’s underlying capacity. Each year, Russia’s public finance system loses more of its resilience. As a result, currency depreciation and other macroeconomic imbalances may eventually make the salary of a “Russian volunteer” far less attractive for participation in the war in Ukraine.

Discuss this article:

-9a7b3a98ed5c506e0b77a6663f5727c5.png)

-c439b7bd9030ecf9d5a4287dc361ba31.jpg "Photo of Katherina Popilnichenko")

")

")